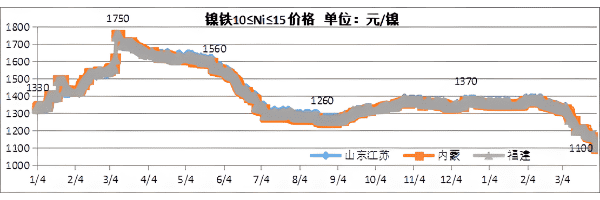

Ferronickel price in different provinces in mainland China

We provide a wide range of square weave wire cloth, woven filter cloth & fabricated mesh in various materials, specifications and shapes to meet different customer demands.

Our woven wire mesh have a wide range of applications, including sieving, filtering & shielding. Just find the product perfectly match up with your applications

Our support center collects all resources we can offer. You can get our data sheets, catalogs and latest news from here and get some valuable information.

Dashang is continuously developing and researching in metal wire and woven wire products. Quality, customer and rapid response are our core competitiveness.

At present, there is an obvious surplus in the supply and demand of Ferronickel, and the power to convert high-nickel Ferronickel to high-Nickel matte is insufficient. The consumption of high-Nickel matte is poor, which intensifies the return of Ferronickel in Indonesia, and the domestic surplus has expanded. However, the output of 300 series stainless steel has entered a low operating rate rhythm from March to April, the demand for Ferronickel is decreasing, and the price of Ferronickel continues to fall. As of the end of March, the domestic mainstream Ferronickel bidding price dropped to 1100–1110 yuan/nickel (including tax to the factory), and this price caused losses for domestic Ferronickel factories. Although Ferronickel production declined from March to April, it was mainly concentrated in domestic independent Ferronickel plants, Indonesia still maintained production. If there is no fundamental change in the level of supply and demand, it means that the price of Ferronickel will continue to approach the Indonesian cost line of 1,030 yuan/nickel, that is, the bidding price of Ferronickel in April is expected to drop to around 1,050 yuan/nickel, or even lower to around 1000 yuan/nickel.

Ferronickel price in different provinces in mainland China

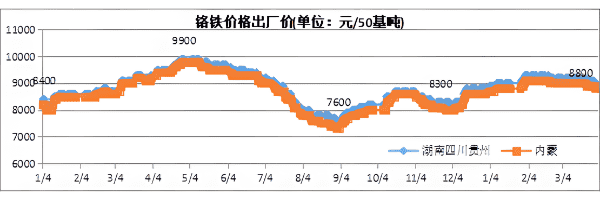

In the first quarter of this year, the price of Ferrochrome showed an overall increase, which accelerated the release of new Ferrochrome production capacity. However, the stainless steel market continued to be weak, and the demand for Ferrochrome decreased, resulting in a loose and surplus domestic supply of Ferrochrome in the first quarter. The output of Ferrochrome in April will remain at about 600,000 tons, while the production reduction of downstream steel factories will continue to expand, and the oversupply of Ferrochrome may further expand, resulting in a slow decline in Ferrochrome prices in April.

Ferrochrome ex-factory price

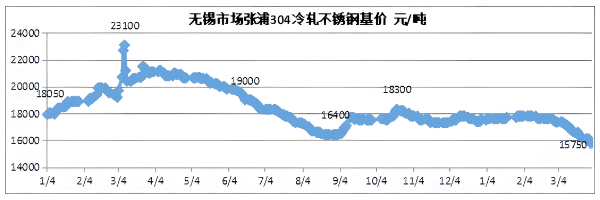

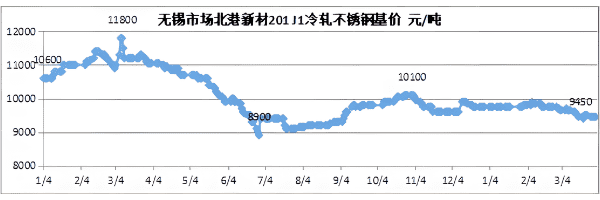

With the multiple pressures of declining production costs, weak demand and high inventory, stainless steel prices fell rapidly in March. As of the end of March, the mainstream of 304 private four-foot cold-rolled resources fell to the range of 14,650–15,100 yuan/ton for raw edges, the mainstream of four-foot cold-rolled resources for state-owned large factories fell to the range of 15,750–16,050 yuan/ton for trimming, and the mainstream of 304 private five-foot hot-rolled slab resources in Wuxi & Foshan fell to 14,600–14,950 yuan/ton for raw edges; the price of 304 cold and hot-rolled plates dropped by nearly 2,000 yuan/ton compared with the price at the end of February. As of the end of March, in terms of 201, the mainstream of J1 four-foot cold-rolled resource in Wuxi and Foshan fell to the range of 9,300–9,450 yuan/ton for raw edges, and J2J5 resources went to 8,700–8,850 yuan/ton for rough edges, which is about 250 yuan/ton lower than that at the end of February. As of the end of March, the mainstream price of 430 cold rolling was reported to be in the range of 7850–7950 yuan/ton, which was about 650 yuan/ton lower than that at the end of February.

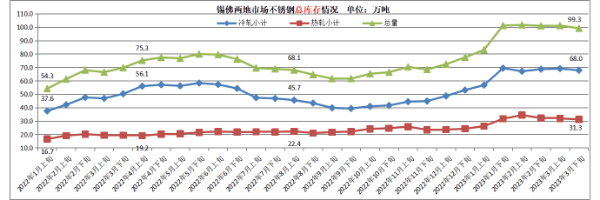

In March, some steel factories experienced maintenance shutdowns, but the effect of reducing production and removing inventory was average. Market inventory remained at a high level, and high inventory has always put pressure on the market. The inventory of steel factories did not decreased, but rather some steel factories increased, indicating that overall demand would continue to be weak.

304 cold rolled stainless steel base price in Zhangpu of Wuxi city

New material 201 J1 cold rolled stainless steel base price in north port of Wuxi city

430 cold rolled stainless steel base price in Wuxi city

Due to the rapid decline in spot prices of stainless steel, the enthusiasm for downstream terminal procurement is currently low, and there is a strong wait-and-see sentiment. It is difficult to maintain only on demand procurement, especially for cold rolled coil plates used for civilian products. In early April, domestic steel factories expressed their intention to reduce production. However, as costs continue to decline, the reduction in production caused by losses will be weaken, mainly due to sales pressure. From the current reduction in production by domestic steel factories, it is likely that the stainless steel market will still be difficult to effectively remove inventory.

In summary, stainless steel raw materials may continue to decline in April, causing the center of gravity of stainless steel prices to rapidly move downwards. With the continuous downward movement of costs, the losses of steel factories have gradually narrowed, and the power to reduce production on a large scale is clearly insufficient. However, the demand recovery is less than expected, and there is a widespread wait-and-see mentality of on-demand procurement in the downstream, resulting in a general shortage of orders from steel factories, which may continue to reduce production and sales. The contradiction between supply and demand of stainless steel in April may continue to be prominent, with limited improvement in inventory pressure, and prices may further decline.

Total stainless steel inventory in Wuxi & Foshan city